Bleeders vs Gappers

Asymmetries in adverse selection

Disclosure: I run Kalshinomics.com, which may earn Kalshi referral fees. I may trade event contracts on Kalshi and securities on other platforms. Readers should consider this relationship when evaluating my analysis. For educational purposes only, not investment advice.

In my last post: “Maker-Taker Math on Kalshi” I discussed how fees impact the decision vs to cross the spread or post a limit, and hinted at the role of adverse selection in having your trades filled. I gave an example of how getting filled at a better price might be a worse trade.

Today I’m going to go deeper into adverse selection with some specific examples from prediction markets.

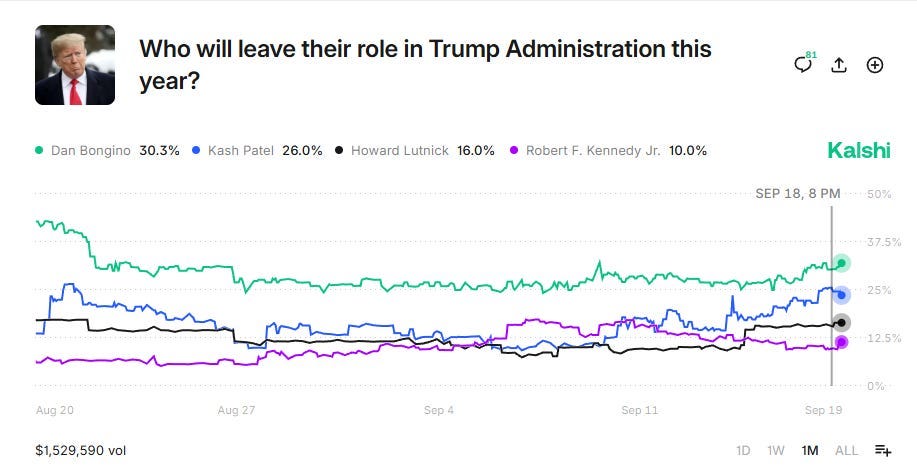

There are a variety of “Will XYZ Event happen this year?” markets, below is one example:

Let’s wrap the very simplest mathematical model we can around the market for RFK Jr leaving [disclosure: as of this writing I am long a small amount of “RFK Jr leaves this year” on Kalshi].

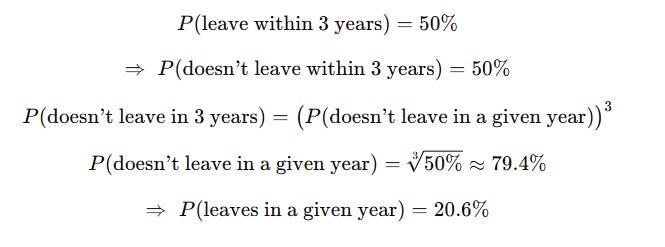

Let’s pretend it’s Jan 1st 2026, and we’re looking at the 2026 version of this contract. We have 365 days to go. We need to estimate a base probability for a cabinet member leaving. We could look at all cabinet members' tenures over the last 50 years, all the cabinet members from Trump’s first term, all HHS secretaries, or we could zoom out and get base-rates for an average worker or average executive in the US. Each one would give us a different estimate.

This concept of data collection and selecting a proper base rate could be an entire series of articles on its own. Additionally after the base rate is selected you need to adjust for the specific individual / role. I have lots more to discuss even drastically simplifying this example - please pardon my lack of rigor and let’s wave our hands and say he’s 50% to leave early, and by that I mean specifically: we assume he’s 50% to leave in the next 3 years, with every day given equal weight. (and again I’m making more simplifications, year 1 does not have to be the same as year 2 or 3 in weight)

Doing some algebra:

To break it up even further let’s go down to a single day. If every day has the same probability, it’s like we’re spinning a roulette wheel every day that has a small chance of hitting “leaves”. If we do that once a day, we have to hit “does not leave” 365 times.

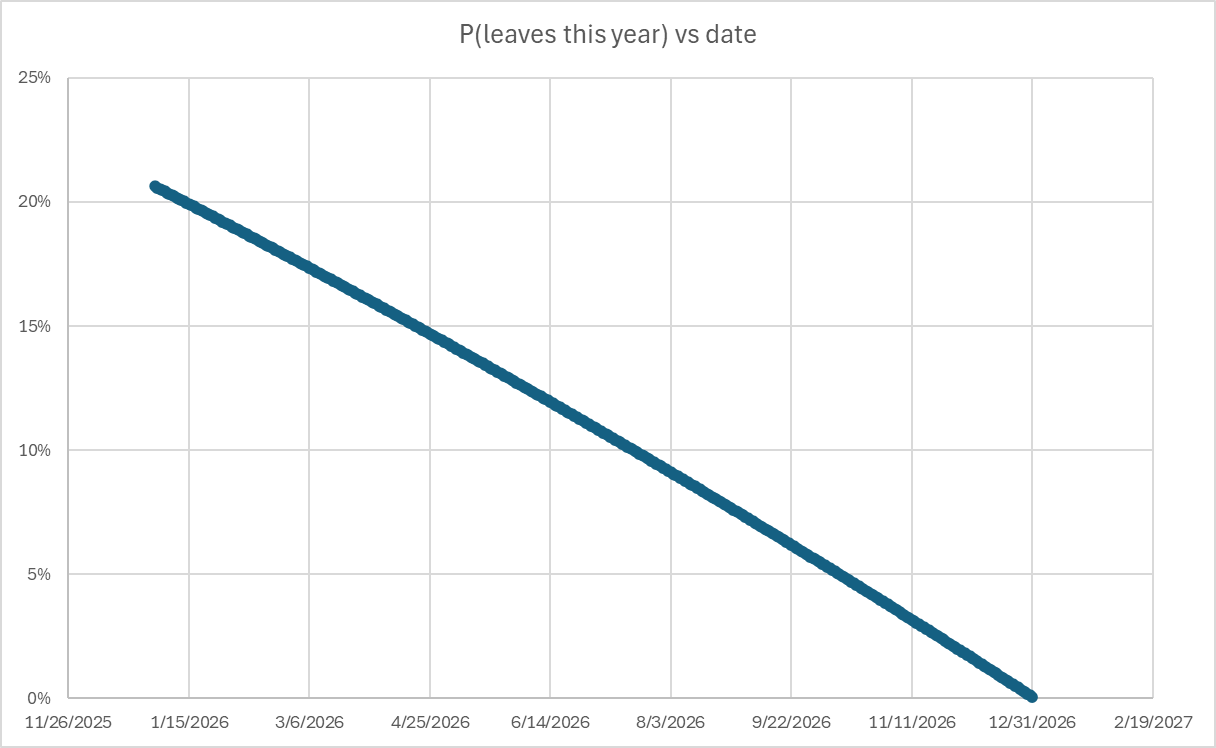

Now we’re moving. Let’s now calculate P(leaves this year, given today’s date). This is slowly go to decay over the year, if there are d days remaining:

This part is straightforward, you come up with a base rate, do some math, and you have a rough look at how the function looks given your assumptions. Models like this are helpful but won’t be enough to beat the market!

Let’s poke at our assumptions:

We could be wrong at the base rate for all positions

RFK Jr might have a very different probability distribution from your average appointee

There’s no reason to believe every day should be equal weighted

This last point about days/time not being equal weighted starts to impose the messiness of reality on our simple model, and the implications become deep, as well as intuitive for understanding the world. (there’s a beauty to me of mixing the math and the mess of reality, this is the same math that applies to options pricing) .

Here are a few intuitions for why we shouldn’t decay all time equally:

Less news is likely to hit on weekends or holidays

Trump is unlikely to decide to fire RFK Jr while he is asleep

P(leaving) is likely higher for the days after contentious Senate Hearings, disruptions in CDC staffing, or new Measles outbreak

You can go very very deep here and build a calendar for every one of the “Who will leave their role in the Trump Administration” markets. Or build a better base calendar. You’re going to want to look for big events or hearings that will either spike P(leave) if they go poorly, or decay even faster if they go well and Trump/Vance offers support.

What I love about prediction markets is that every event type is going to have its own calendar, and those calendars tell you something about the state of the world. Here you’re looking at the Senate calendar and CDC news, vs on markets like “How many Atlantic Hurricanes will there be this year” you’re studying weather patterns and their distribution across time

Bringing it back to adverse selection:

Reintroducing Noisy Nick and Sharp Steve. Noisy Nick trades randomly every hour with no information, Sharp Steve knows exactly what the price is worth, has an infinite bankroll, is extremely fast to trade on new information, and only does good trades.

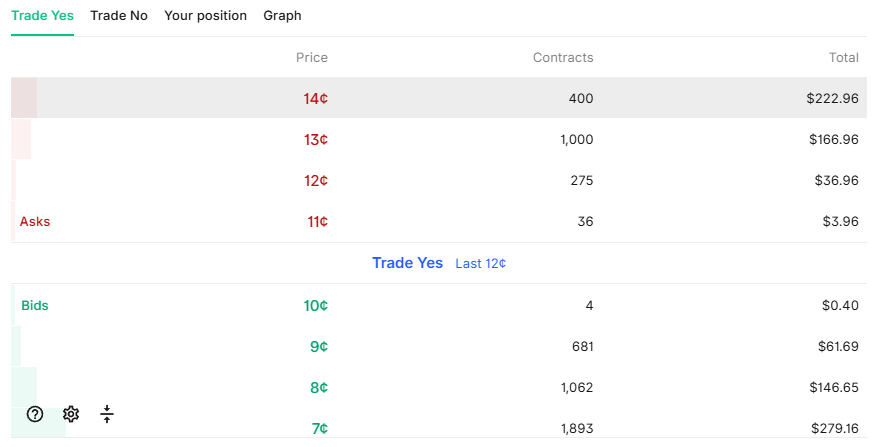

Here’s the “RFK Jr Leave” orderbook:

So it’s right around 10%, given this market “Will RFK Jr leave this year”, we need to ask ourselves “What could Sharp Steve know?”

He might know things like:

Trump is going to make public statements expressing support for RFK Jr (private information)

Trump just tweeted positive support (public but breaking news)

Thousands of HHS services just signed a letter against RFK Jr (private information)

A new disease outbreak just hit due to low vaccination rates (private information)

Trump just agreed to fire RFK Jr and is about to announce it (private information)

Trump just announced he’ll fire RFK Jr (public information)

Today’s senate hearing is going well for RFK Jr (interpretation of public information)

[Note: This analysis explores theoretical information advantages for educational purposes. In practice, trading on material non-public information may violate securities laws or platform terms of service. I am considering the entire set of information an individual “could possibly know”]

In some cases Sharp Steve could have information that is not known to the wider market, in others the information is public but Sharp Steve is very fast. If we have a limit order out in the book - it doesn’t matter which, Sharp Steve is going to trade before we see the info and cancel the order. This provides one hint to our strategy -> if we know an event is coming up that may swing the odds in either direction - we need to cancel our limit orders BEFORE the event.

Some of the events are positive for RFK Jr, some are negative, but think about the magnitude in either direction. The contract is trading around 10%, even if there is good news for RFK Jr, with time left on the clock for any human in any job, the chance of leaving is not zero. The contract can only move some amount lower before base rates kick in. Most of the time, this contract is going to bleed lower as time passes.

However, Sharp Steve could know precisely that RFK Jr is about to be fired. The contract is about to gap higher to close to 100%. The significance of Sharp Steve’s information is not symmetric around the market price.

If you have a 10¢ limit bid and you just got hit by Sharp Steve, how bad is your trade on average? He probably knows there’s good news for RFK Jr, or has a better decay schedule, maybe the contract is worth 8¢ or 9¢, your trade might be bad by an average of 1.5¢. With some knowledge of the decay schedule you can avoid leaving out bids that will easily be picked off due to the passage of time.

If you have a 11¢ limit offer and get lifted by Sharp Steve, your trade could be as much as 89¢ bad! But at least your order is at the level of the best offer, at this price you may also interact with Noisy Nick.

This gives us another hint at what not to do -> don’t leave out resting orders in newsy time periods, especially in the direction of gap risk. Don’t leave large resting orders at higher prices without paying attention. Let’s say you have a 20¢ offer and you’re not paying attention, it’s been posted for a week. All of a sudden you get lifted… What do you think just happened? Either a price insensitive buyer just paid way over the previous offer… or impactful news just hit and you did an awful trade against Sharp Steve.

Note this can’t happen the other way, if you have a 5¢ bid and the market is 10¢, there’s very few headlines that can make buying immediately awful, there’s a natural bleed to the passage of time.

This type of "Will an individual leave?" market is not the only one with gap risk. "Which company will announce an IPO this year?" represents a category where information asymmetries can be extreme, there is limited publicly available information outside news reports and speculation, while those closer to the decision-making process may have superior information about timing and likelihood. This creates significant adverse selection risks. There are individuals that can know the chance is near 100% or 0%, as well as breaking news that can provide this information to the market faster than our chance to react.

In election markets it is hard for anyone to know they’re going to win the election. But it is possible to know if someone is going to drop out of a race, is sick, has a scandal etc. Each market has its own distribution of gap type events and some type of decay calendar.

How do I apply these ideas in practice? For one, I’m just a hobbyist trader (though previously was a pro in ETFs), I don’t trade huge size and have little market impact with my orders. I avoid having limit orders posted for extended periods in general, but especially on the gap side. I send orders that are small vs the average daily volume of the contracts, and I keep them near the top of the book. If the market goes my way I don’t keep the order out. On Kalshi you can set an expiration time on each order, keep it short.

Request for Feedback

What other prediction market prices show this asymmetry in short term moves?

I’m happy to hear any feedback on my writing or ideas for other pieces. There’s lots of great finance / decision-making writing out there but the prediction market space is expanding quickly - it’s exciting to see. I understand the sports side is huge for business - but I’m most interested in markets that provide a social good through their pricing - election markets, geopolitics, economics. I believe these markets are a great tool for self education on math, probability, and the difference between reality vs quantitative modeling.

I’m also planning on organizing a prediction markets meetup in Philly in October. If you read this and are interested shoot me a msg.

If you’re an expert please point out any mistakes I made in the analysis! And if you’re a beginner please let me know if any of the terms I use are confusing.

Do you think there is a way to quantitatively model the difference between sharp Steve and noisy Nick? Or is this be something that is more intuition based on the guidelines you presented?

Great post! Domer mentioned that he spent lots of time monitoring news when he put up tight limit orders to earn the liquidity rewards. Avoiding news related adverse selection is critical in liquid markets. Anecdotally, there are niche markets that get hit with one or two big uninformed trades which remove the already thin liquidity, so there is a balance between being prudent and not missing out on very good fills.